Why Does George Weston Remind Me of My Old Dog “Smoke”?

And two words worth remembering for the rest of your life.

When I was a kid, we had a dog named Smoke. A big Gordon Setter. Sitting still, he cut a stately figure. Turn your back for ten seconds and he was known to eat an entire pizza off the counter.

Lately he reminds me of George Weston. Let me introduce them both a little better.

George Weston was a bread-maker who opened his first bakery in Toronto in 1884. His name now sits atop George Weston Limited, the holding company that controls Loblaw, Canada’s largest grocer. The same family, through a separate British arm, owns Primark, Fortnum & Mason, and pantry staples from Twinings to Silver Spoon. They are among the richest families in Britain. The name is printed on the storefronts, and on the bread itself.

Smoke, the dog, was loyal, gentle, and a great companion. But given ten unguarded seconds, he’d take your dinner. Regal in some regards. Impulsive in others. I can still see him in the doorway of the kitchen, the entire extra-large pizza clamped in his mouth, pepperoni and tomato sauce dripping on the floor, right before he inhaled it all.

A retail dynasty worth more than a king. A setter with a stolen pizza. On the surface, nothing in common, and yet, lately, I cannot stop seeing one in the other.

Next week I'll explain why in detail, connecting the dog to the tycoon. The trailer to this story is the $47.11 cheque I just received in the mail from the Westons. It came with a letter that reads:

“This payment represents your share of the Loblaw/Weston Packaged Bread Settlement.”

What can a class action lawsuit and a half-trained dog teach us about multi-billion-dollar companies?

To get there, we need to first explore a major concept in Supplierism. It may sound like homework. But it is also the cheat code to capitalism. If you buy anything, from anyone, ever, this affects you. This part deserves your attention, two words worth remembering for the rest of your life:

Contingent Liabilities

The International Accounting Standards Board defines a contingent liability as a possible financial obligation arising from past events, whose existence will be confirmed only by some uncertain future event. In other words, accounting language for a bill that might come due later, depending on how things play out.

Boring? Yes. But possibly the most consequential mechanism in market capitalism.

Every harm a company creates is a contingent liability: the carbon it emits, the privacy it erodes, the corruption it funds, the labour it exploits, the safety it cuts, the children it hurts, the truth it fails to report. Understand this one concept and you understand how the largest harms on Earth stay hidden until it is nearly too late.

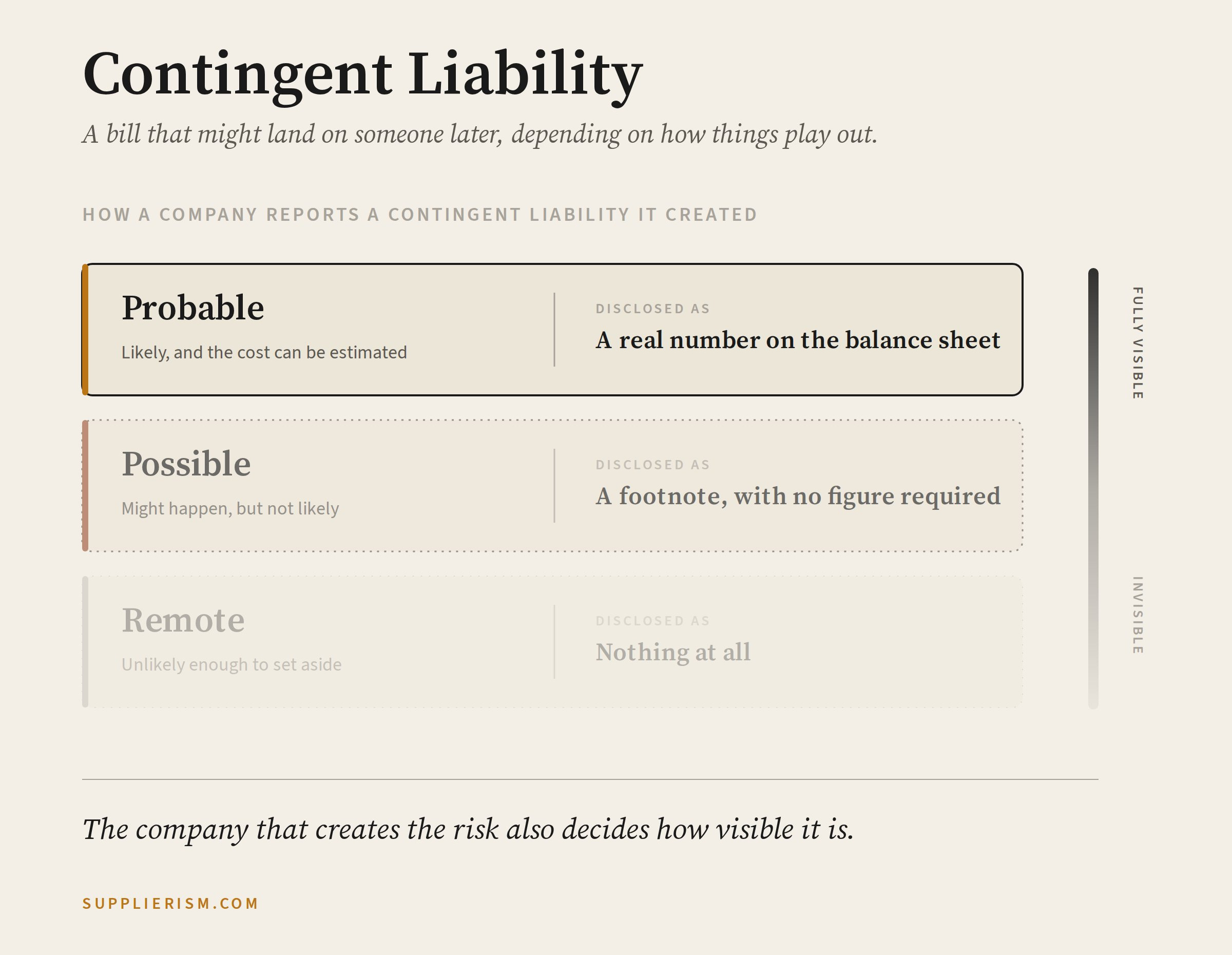

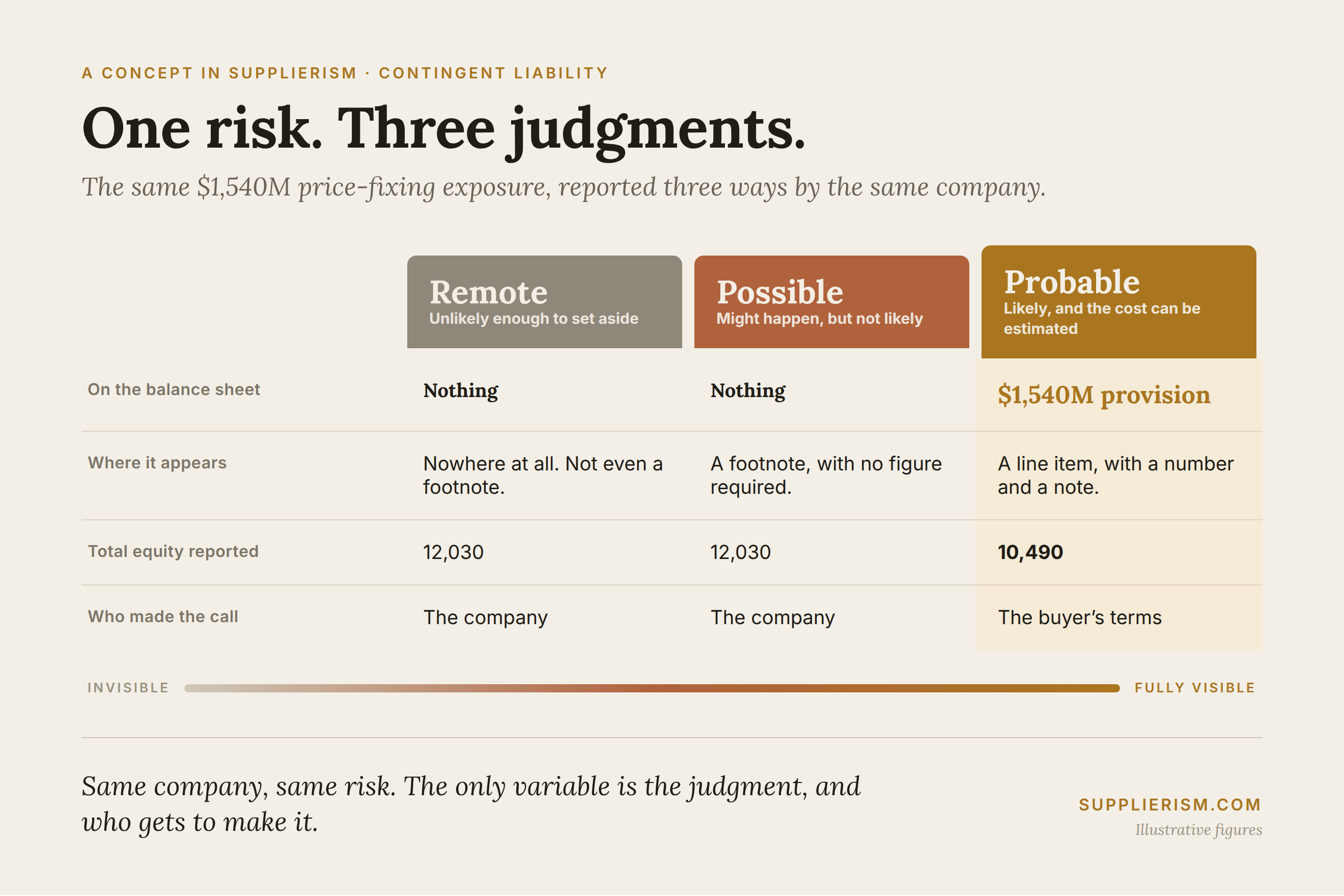

Exactly how a corporation reports a contingent liability depends on its probability, which the company itself judges. If the cost is Probable and can be estimated, it goes on the company’s balance sheet as a real number. If it is merely Possible, it need only be described in a footnote, with no financial numbers required. If it is deemed Remote, it need not be disclosed at all. All of this is signed off by CEOs and their boards in audited financial statements.

For the vast majority of harms they create, corporations report their share of the liability as "Remote," a classification that requires no disclosure and so escapes auditor scrutiny. In other words, the company creating the risks that may harm you and your family also gets to decide whether those risks stay invisible to investors, insurers, banks, regulators, and you.

Our world (and the one we leave our kids) pivots on contingent liabilities

An astonishing amount of the world's economic power changes hands the moment a contingent liability is assigned or extinguished. One of the central jobs of corporate finance is to push these liabilities off the company's books, onto the customer, the worker, the regulator, the planet. Your kids, and your kids' kids.

Here's the part that's easy to miss. Every single thing you buy comes with a contract. Buy a fire extinguisher that fails when you need it, and you clearly have a case against the manufacturer. Buy a pack of gum you don't like, and you can still try to sue. You'll likely lose, but the fact that you can file a complaint at all means you entered into an agreement when you bought it. The law calls this an implied contract: one created not by signatures but by conduct. You handed over money, they handed over goods, and that exchange alone binds both sides.

Digital commerce has been a boon for corporations. Online, the implied contract gets replaced by lengthy legal agreements buyers must accept before they finalize a purchase. The whole system is currently lopsided in favour of suppliers. But here's the key point with both implied contracts and digital ones: the relationship between you and your supplier is governed by commercial contracts.

When a supplier creates a future cost and quietly passes it to you, they create a contingent liability that goes unreported. Think of the seven tobacco CEOs who swore to Congress in 1994 that they did not believe nicotine was addictive, while their own files, going back to the 1960s, said plainly that it was. The harm was real and already in motion. It simply lived with the smoker and the public health system, not on the company’s books.

The Facebook whistleblower Frances Haugen revealed the same pattern in 2021: internal research showing the company knew its product was harming teenagers, especially girls, while it said nothing publicly. The lawsuits, the regulation, a generation harmed on its watch: the liability was floating off the books, possible but not yet probable, until Haugen made it real.

Capitalism is a continuous contract negotiation about where contingent liabilities sit. Who owns them. How they are reported. When it becomes cheaper for the company to fix the liability rather than hide it.

Regular buyers like us can't easily negotiate with our suppliers. The current system is backwards: we pay first, and find out about the hidden costs later.

Think of General Motors. For more than a decade, GM knew the ignition switches in millions of its cars were defective; the switch could slip out of position mid-drive, cutting the engine and disabling the power steering, brakes, and airbags. The fix would have cost 57 cents per car. GM left it in place. By the 2014 recall of 2.6 million vehicles, its own fund had tied the defect to 124 deaths and 275 injuries. GM paid more than $1.5 billion in settlements and fines to resolve a problem it could have fixed for pocket change. That bill was a contingent liability the whole time, sitting off the books, carried by drivers who didn't know their airbags might not deploy, until their deaths made it impossible to ignore.

In Supplierism, your values become impossible to ignore when shared across a large group of buyers. Women, for example, control an estimated 70 to 80 percent of all consumer spending, the single largest buying bloc on earth. And yet this year the New York Times ran "Buckle Up, Women. Cars Still Aren't Built for You," reporting that women are 17 percent more likely to be killed than men, and 73 percent more likely to be seriously injured in a head-on crash, because vehicles are still designed and crash-tested around a "default" male body. The most powerful buyers on earth, and in 2026 the product still isn't built for them.

The cost of every woman injured or killed because the car was built around a man’s body is a contingent liability that exists today, but appears nowhere on the carmaker’s books, because no one negotiated for it to sit with the company rather than with you (or your mother, daughter, sister, partner).

Correcting bad corporate behaviour isn’t about punishment. When a contingent liability sits on the books of the company that created it, the incentive flips: it becomes cheaper to prevent the harm than to carry its cost. That’s a reward system, one that trains your suppliers to be good. In capitalism, there is always negotiation. Supplierism is simply better capitalism, a version where regular customers hold most of the leverage. Enough to set terms like these, before you hand over your money to a car company:

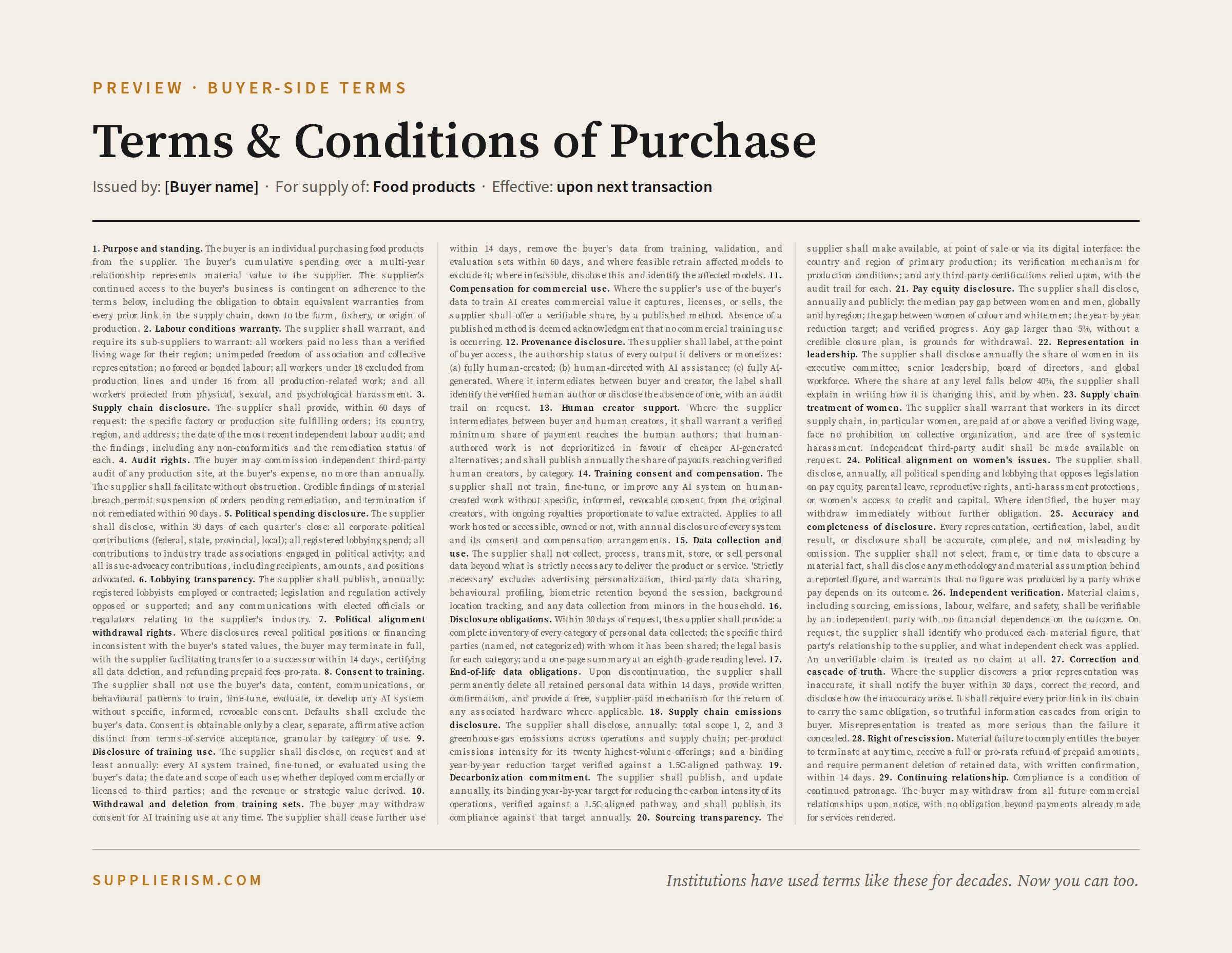

The supplier warrants that this vehicle was crash-tested for driver safety using a model based on female anatomy, not a scaled-down male one, and will disclose any gap between its female and male injury-risk results at the point of sale. Failing to test for female safety, or to disclose the results honestly, is a material breach of this contract.

The same idea applies to a loaf of bread. Those terms might read like this:

The supplier warrants that the price of this essential food was not fixed in collusion with competitors, and that its labour practices and political spending are fully disclosed. Colluding on price, or concealing any of these facts, is a material breach of this contract, subject to penalties.

In reality, the supplier would be reading something more detailed, like the contract below, generated by you in seconds:

Did you read every line of that? Probably not. And it doesn't matter. The point was never that you personally read the fine print. The point is that your supplier does.

When acceptance of your terms is a condition of the sale, the contingent liability goes onto the supplier's books (if they're violating any of your terms).

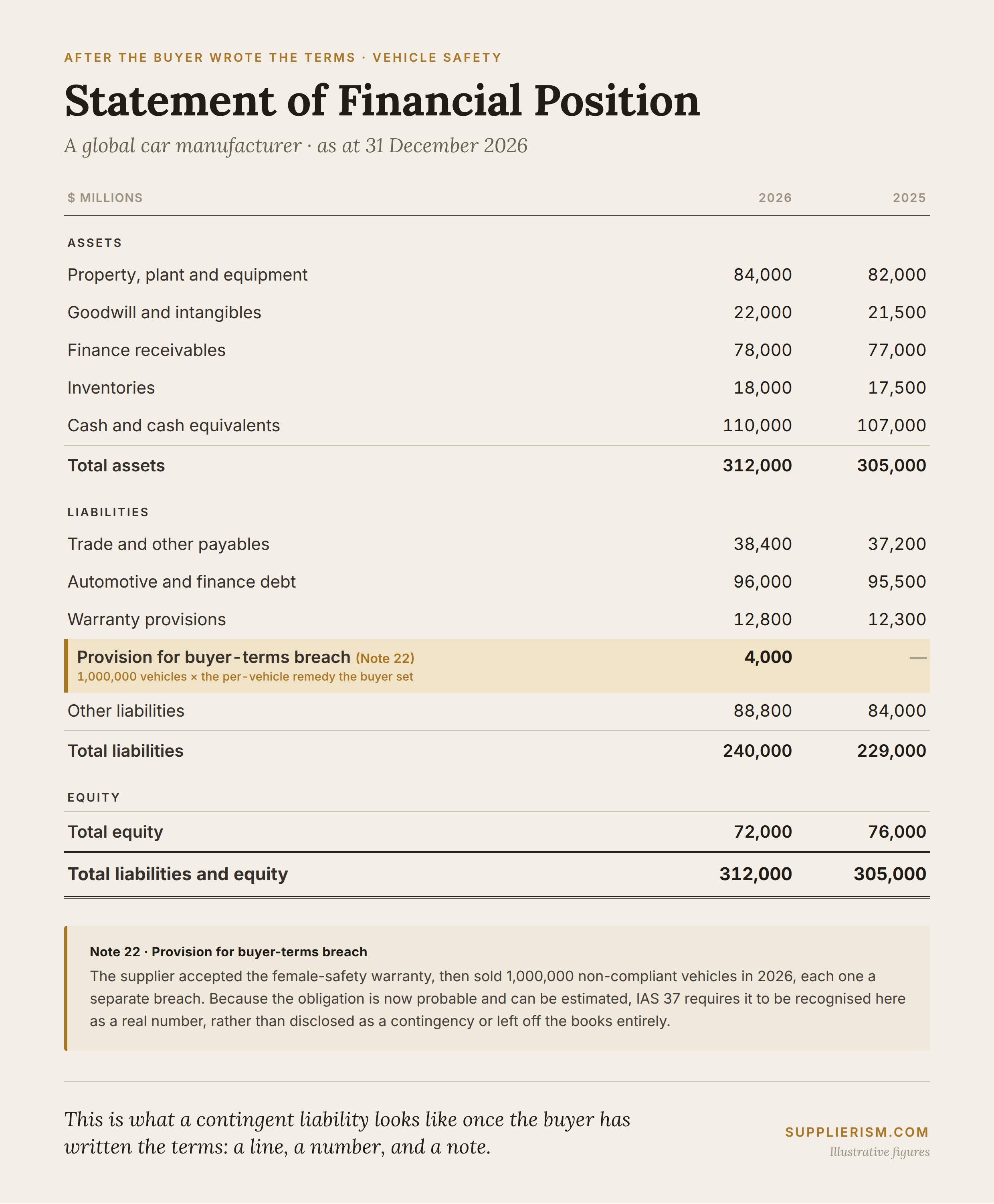

To show what that actually looks like, I built financial statements for a fictional car company. Here’s the picture when that supplier is forced to own the liability for selling one million unsafe cars:

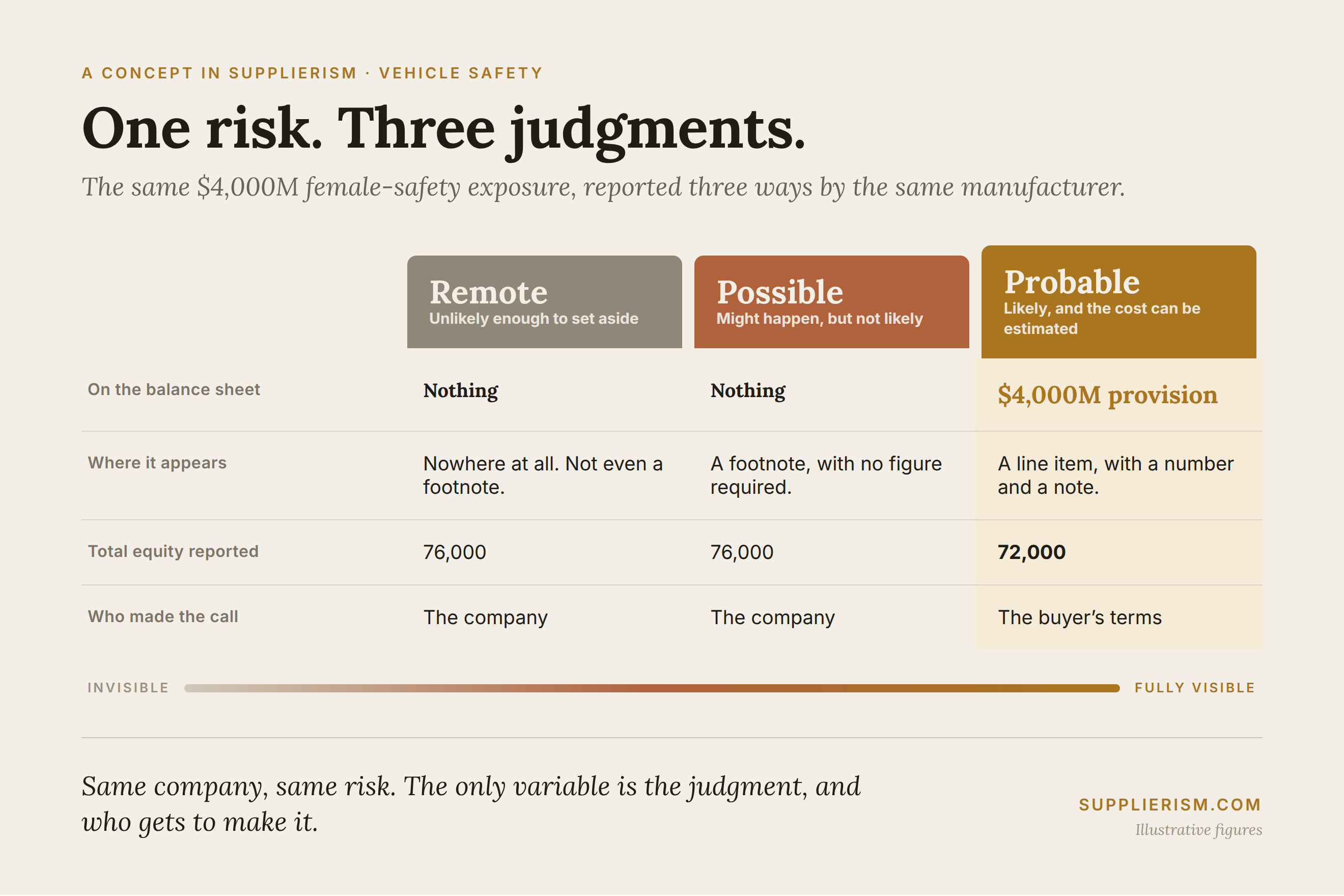

Compare the three ways this fictional car company might report its contingent liability. Only the "Probable" treatment puts the harm on the balance sheet as a real cost. The other two keep it off the books entirely.

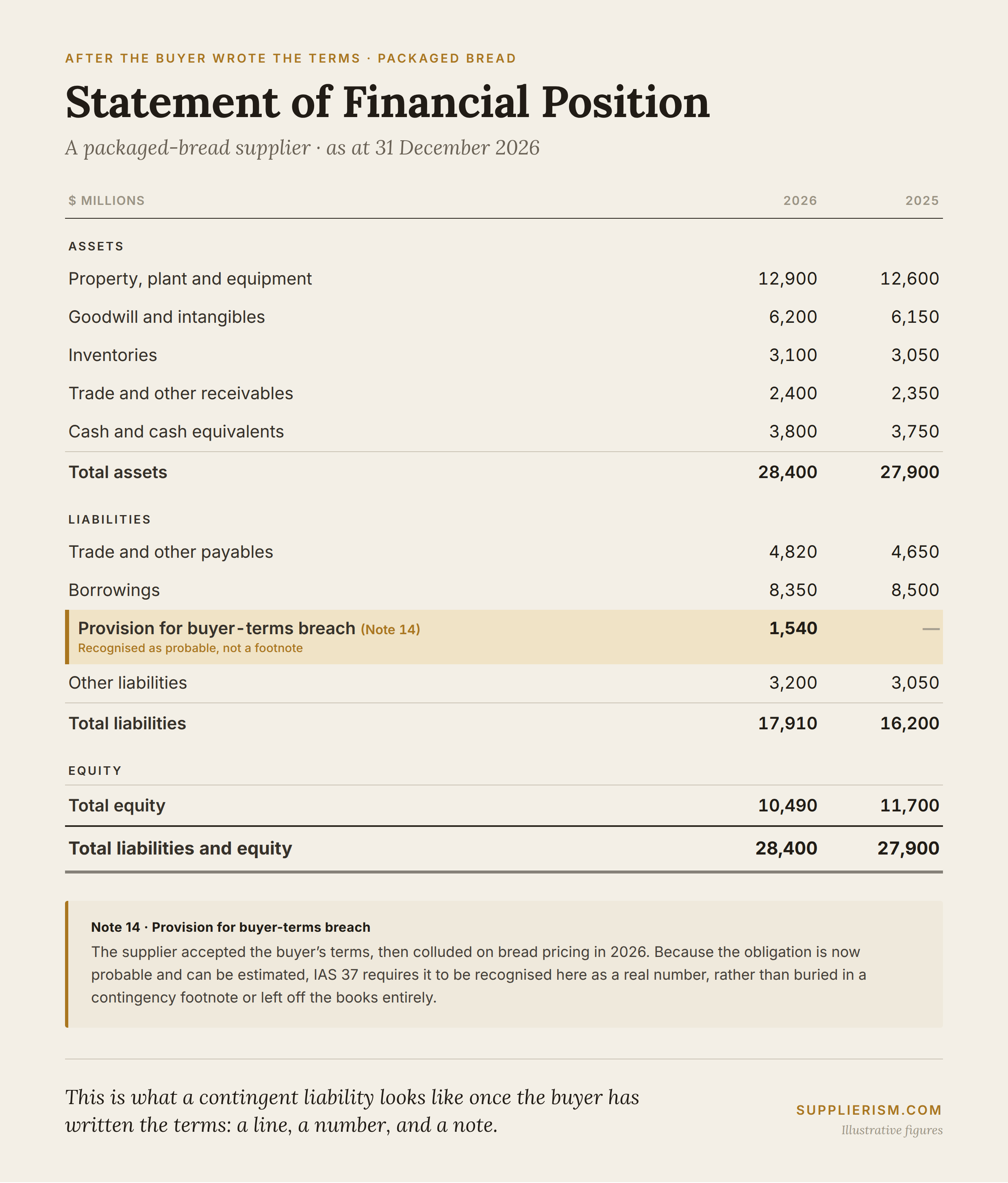

I also created financial statements for a fictional bread company. Here is what it looks like when that bread supplier is forced to own the liability for colluding to fix the price of an essential food:

Again, the "Probable" treatment is the only one that forces the company to account for what the collusion actually cost its customers.

In both the car and bread cases, once the liability is deemed "Probable" it lands on the company's balance sheet. The supplier either fixes the underlying problem or wears the consequences: lower share prices, smaller executive bonuses, a weaker ability to borrow money. Those fall on owners and managers directly, which is exactly what drives better behaviour.

That's the leverage Supplierism gives you. When buyers insist suppliers own what they create—the carbon they emitted, the privacy they violated, the corruption they funded, the labour they exploited, the safety they cut, the children they hurt, the truth they failed to report—the cost finally sits with the company, not with you.

Managing contingent liabilities was designed to be boring, unglamorous, and deliberately complex. That's part of what keeps the leverage with large corporations, who staff whole departments to make sure the cost ends up on your balance sheet, not theirs.

We are building the tools to change that: a free, automated terms generator meant to sit on every phone, negotiating for you. You can try building your own terms and conditions here: supplierism.com/demo. And if you want to see how we get from awareness to execution at scale, the roadmap is here: supplierism.com/building.